Tengo la manía tonta de querer entender mejor las cosas que me afectan. Después de sumergirme en el cálculo del sueldo neto, con su correspondiente calculadora, la cúal nunca esta lo suficientemente actualizada como bien se encargan de recordarme cada vez que hago algo de SPAM. Estos últimos meses he estado trabajando en una calculadora de la cuota mensual de la hipoteca. O en corto, que tiene mejor SEO:

Tengo una hipoteca desde hace un año y medio y es todo un mundo. Cuando empecé a buscar bancos y preguntar a amigos te das cuenta de los mitos y creencias. Los que más me sorprendieron fueron:

Los “variablelivers”

En el momento que contraté la hipoteca, los tipos estaban por los suelos y llevaban años así. Se podían conseguir hipotecas tipo fijo a 1 y pico % de interés. Pues aún así muchos amigos me recomendaban variable. Los variablelivers decían su mantra: “¡El euríbor no va a subir!”. Que rápido se les ha complicado la cosa…

Valor histórico del euríbor

| Año | Valor |

| 2022 | 3,018% |

| 2021 | -0,487% |

| 2020 | -0,481% |

| 2019 | -0,272% |

| 2018 | -0,147% |

| 2017 | -0,189% |

Amortiza siempre!

Otra fauna muy común, tiene un mandamiento que pregonan: “¡En cuanto ahorres algo amortiza!” “¡Tienes que quitarte el préstamo cuánto antes!”. A ver, no siempre. Y para muestra mi propio caso. Mi hipoteca es 1,6% tipo fijo. Mientras escribo estas líneas hay dépositos al 2%. Gano 0,4% anual sin riesgo. ¿Amortizo? ¿De verdad? luego esta la inflación, todo será más caro dentro de 30 años, también cobraré más (espero) pero, ¿la cuota mensual? será la misma. Al final lo de amortizar es sencillo, si tienes el dinero muerto del asco en la cuenta, amortiza. Si le sacas mejor rendimiento que los intereses de tu hipoteca, no amortices.

Los que tienen un tipo bajísimo. Maestros negociadores.

Finalmente, también me encontré alguno que tenía tipos muy muy bajos y yo sorprendido, ¿cómo lo habrán conseguido? A la que rascas un poco se descubre el pastel. Tenían contratado con el banco hasta ¡la alarma de la casa! Seguro de casa, alarma, seguro de vida, seguro de pagos, ¿quién da más? y estos seguros metidos en la deuda total, para cobrar sus buenos intereses también sobre ellos. El coste real de la hipoteca mes a mes era muy diferente al de contabilizar solo el tipo de interés. Hablaré de eso más adelante pero spoiler: los seguros que ofrece el banco son más caros y peores (combo).

Sea como sea, si lo que te comento te suena a chino, quédate y intento resolver tus dudas. Abre la calculadora de hipoteca en otra pestaña del navegador y ve jugando.

Prestamo francés 🇫🇷

Las hipotecas en España son del tipo préstamo francés. La gracia de este tipo de préstamo es que las cuotas son las mismas durante toda la vida del préstamo, lo que ayuda a evitar imprevistos etc. Eso los ha hecho los más comunes. Esto me lleva a otro mito muy extendido. “En las hipotecas se pagan muchos más intereses al principio que al final” y bueno si es cierto que se paga más pero el único motivo es porque debes más! Si la cuota siempre es la misma y tú al banco al inicio le debes TODO es normal que pagues más intereses, vamos con un ejemplo para entenderlo mejor.

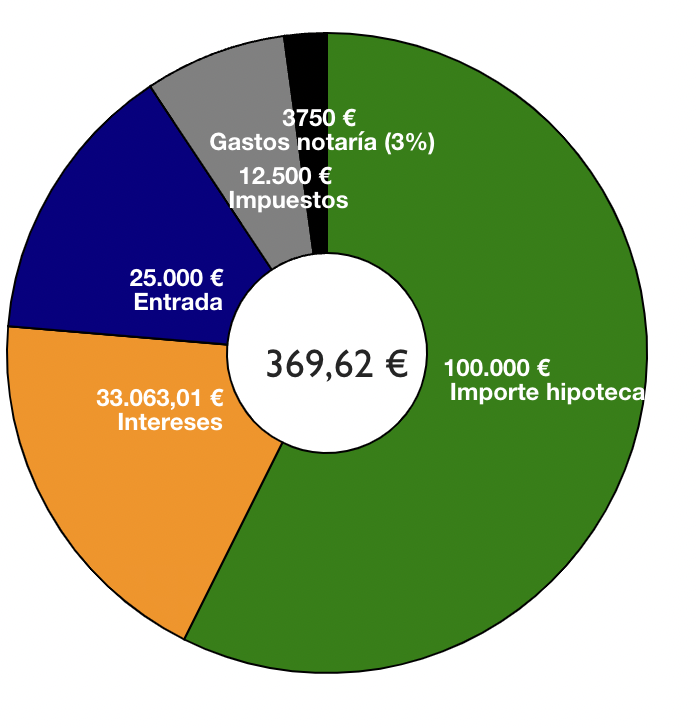

Imagina un préstamo de 100.000 a 10 años, con un interés del 1%. Números redondos para facilitar cálculos. Los intereses son anuales así que el primer año le tienes que pagar al banco el 1% de 100.000€. Es decir 1000€ euros. Dividido entre 12 meses, 83,3€ mensuales. El resto de cuota es la deuda que la vas reduciendo, en este caso 876,04€ - 83,3€ = 792,74€ mensuales. 9512,88€ anuales.

Ahora vamos al año dos. La deuda es ahora el resultado de restar la dueda inicial menos lo pagado el primer año, es decir 100.000€ - 9512,88€ = 90.487,12€. Los intereses del segundo año son entonces el 1% de esa cifra, es decir 904,87€. Cada mes solo 75,41€. Ha bajado unos 8 euros con respecto al año anterior (83,3€). ¿Se ve la tendencia? Cada año pagas menos intereses porque vas reduciendo tu deuda.

La entrada

Por norma general, el banco te va a dar una hipoteca de como máximo el 80% del valor de la vivienda. Este valor se obtiene mediante tasación. Si el precio de venta es menor al de tasación se usará ese valor. Siempre el mínimo de esos valores (venta o tasación). Además el 80% se da si es tu primera vivienda, donde te vas a empadronar. Para una segunda vivienda el máximo valor de la hipoteca es 70%.

Tipo fijo, variable o mixto

Cuando contratas la hipoteca puedes escoger tipo fijo o variable (mixto es una mezcla de ambos). Tipo fijo, como el nombre indica, se decide al inicio del préstamo y ya no cambia más. Solo puede cambiar si tienes bonificaciones por domiciliar nómina, etc. y dejas de cumplirlas.

Tipo variable depende del famoso euríbor. No voy a entrar al detalle de que es el euríbor, pero tomalo como un índice de referencia que puede subir o bajar y los intereses de tu hipoteca dependerán de ello. Por ejemplo imagina que tienes una hipoteca que tus intereses son “euríbor + 0,5%”. Pues si el euríbor esta a 3%, tu intereses anuales serán 3,5%. Normalmente se recalculan los intereses cada 6 meses o cada año.

La pregunta del millón, ¿cuál es mejor? la respuesta depende del contexto económico general y de tu caso particular. De antemano nadie sabe cual va a ser mejor así que toca un buscar el riesgo de la variable o a tranquilidad de la fija. Piensa además que puedes cambiar la hipoteca a otro banco durante el préstamo. Imagina que contratas una hipoteca a un tipo fijo alto y luego baja mucho el euríbor. Los bancos empezarán a ofertar hipotecas con mejores condiciones que la tuya, puedes cambiar. Se le llama subrogar. También es probable que si tu banco le enseñas que te vas te mejore las condiciones.

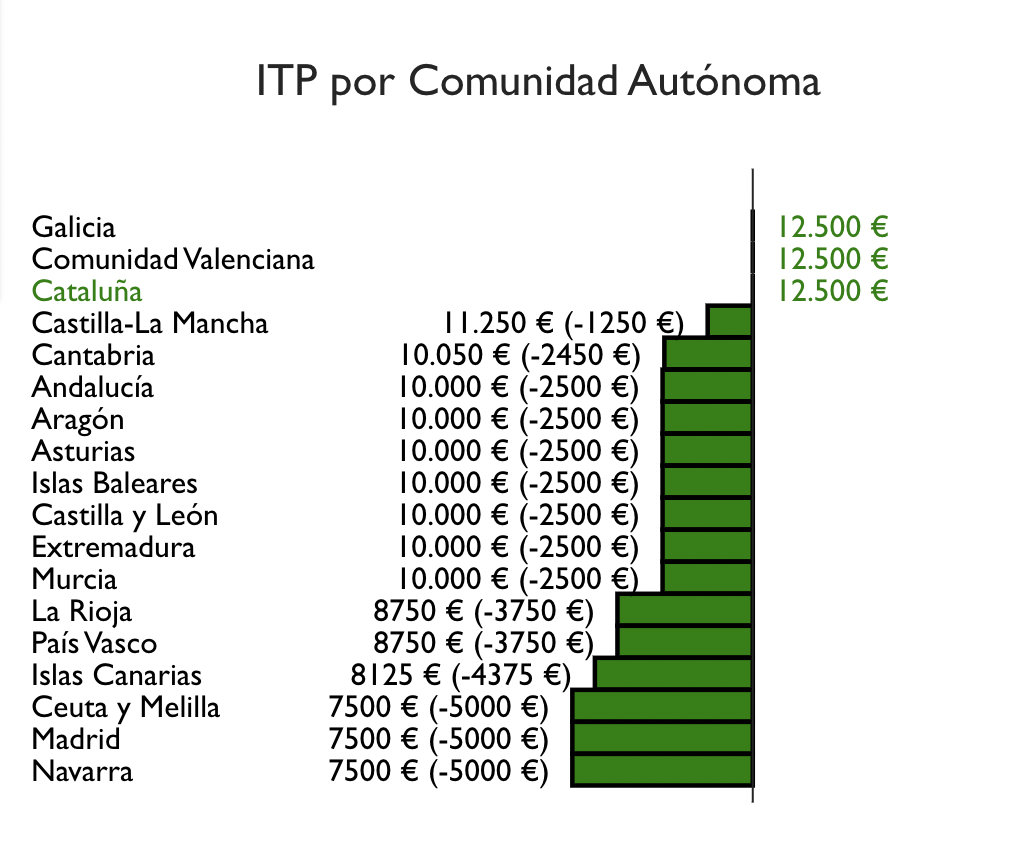

Impuestos por compra de vivienda IVA o ITP

Dos cosas hay seguras en la vida, la muerte y los impuestos. ¿Que pensabas que no pagarías impuestos por comprar una vivienda? Pues claro que sí y no pocos. Si la vivienda es nueva es fácil, es una 10% de IVA. Si la vivienda es de segunda mano ya se complica la cosa. Como con el IRPF cada comunidad hace y deshace a su antojo y vuelve a ganar Madrid con solo un 5%. Muestro una comparativa por comunidad y los impuestos de todas las comunidades en un tab de la calculadora.

Notaría y otros gastos

Finalmente, hay gastos de notaría, gastos de la inmobiliaria si usas una, etc. Es muy difícil estimar porque depende mucho del caso. En la calculadora he puesto un 3%.

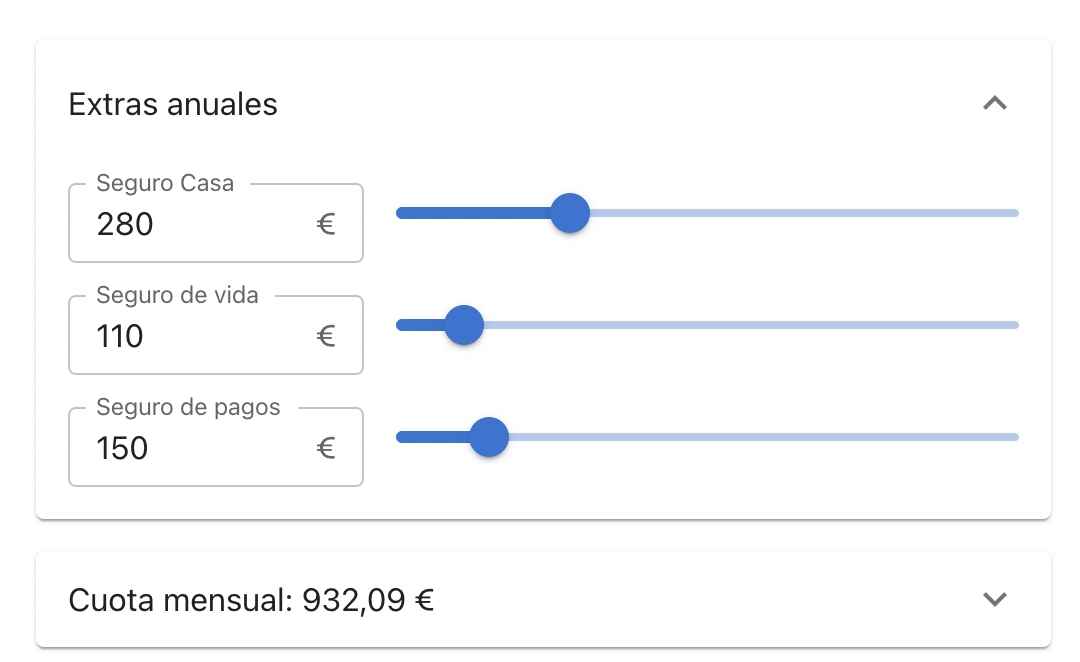

Seguros de saludos, vida, extras, compara bien

Hasta aquí hemos visto los gastos obligatorios. Pero el banco siempre quiere más. Al ganar tan “poco” con la hipoteca buscan colocarte varios seguros. Estos seguros te bonifican y te bajan tu tipo de interés. Hay que hacer números, no os precipiteis y calculad si vale la pena. En la mayoría de ocasiones es mejor contratar los seguros (si los necesitas) por tu cuenta. El único seguro obligartorio es el de la casa, ninguno más. En mi caso, me obligaron a contratar el seguro de casa el primer año con ellos. Al año siguiente lo dí de baja y conseguí un mejor seguro con más de 100 euros de ahorro. Repite conmigo, hipotecas en bancos, seguros en aseguradoras.

Lo que estoy seguro que no vale la pena nunca es poner los gastos de los seguros de todos los años dentro del préstamo de la hipoteca. Vas a pagar unos intereses inecesarios. Para facilitar los cálculos te pongo este apartado en la calculadora donde puedes ver como afectan la cuota mensual estos seguros extras.

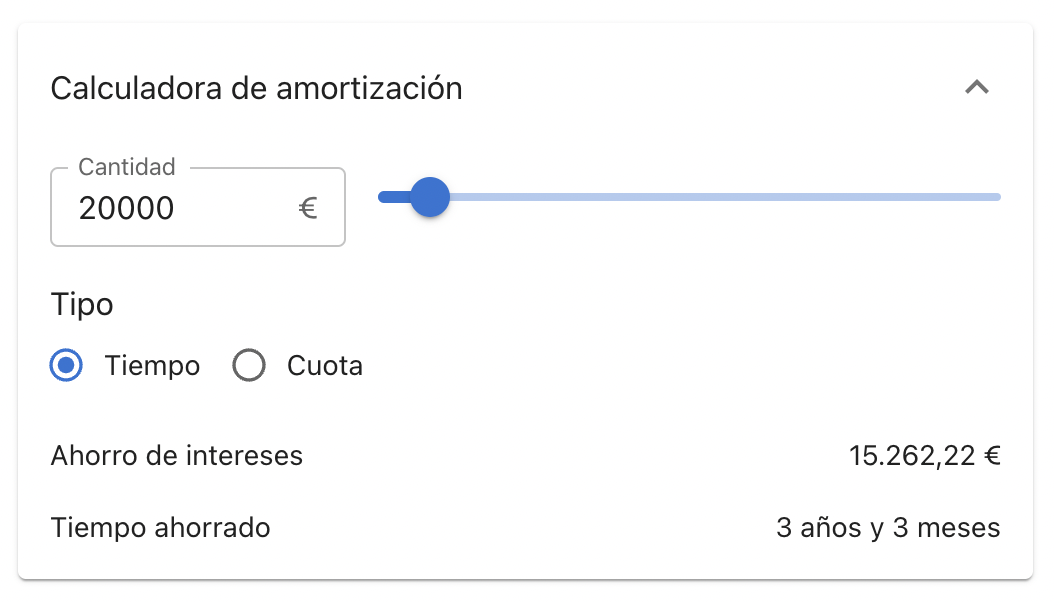

Amortizar

Amortizar es adelantar pago de tu deuda para que esta sea menor. Hay dos tipos de amortización. Una opción reduce la duración del préstamo (menos meses) y la otra opción reduce la cuota mensual. La opción con la que se ahorran más inteses es con la de reducir duración del préstamo pero va a gustos. Quizá interesa reducir una cuota muy alta que nos lleva ahogados. En la calculadora se pueden comparar ambas opciones

Conclusión

Hasta aquí esta breve introducción a la hipoteca. Es posiblemente el préstamo más importante que contrata una persona en su vida, que menos que entenderlo bien.

]]>